Privacy Focused Infrastructure and Ai Development

You Will Own NOTHING And Be Happy? Part 1 of 3

How Did We Get Here?

The Century of Corporate Consolidation (1830-1945)

The Architecture of Economic Control

Look, if you want to understand why you can't afford anything, why everything's a subscription, and why a handful of corporations control basically the entire economy, you need to go back. Way back. We're talking 1830s America, when corporations were still these weird legal entities that most people didn't trust, and for good reason.

Here's the thing we don't learn in history class: the economic system screwing over young people today didn't just happen. It was built, piece by piece, over nearly two centuries. Each generation made decisions that seemed reasonable at the time but laid the groundwork for the next level of consolidation. By the time you get to 2024, you've got this towering architecture of control that looks natural but is actually the result of very specific policy choices.

So let me walk you through how this happened. And I'm warning you now, once you connect the dots, you can't unsee it.

The Railroad Era: When Corporations Learned to Capture Government

Before the Civil War, Corporations were considered public servants (sort of).

In the early 1800s, corporations were different animals. You couldn't just file some paperwork and start one. States chartered them for specific public purposes. You wanted to build a bridge? Fine, here's a corporate charter, but it expires in 20 years and you have to maintain the bridge for public use. The whole idea was that corporate privileges (like limited liability) came with public obligations.

But then came the railroads.

The Pacific Railway Acts of 1862 and 1864 changed everything. The federal government handed railroad companies 170 million acres of public land. That's an area larger than Texas. Plus $64 million in government bonds. Just gave it to them. The justification was that the country needed transcontinental rail, and private companies were the ones to build it.

Seems reasonable, right? Except here's what actually happened: these companies got the land, built the cheapest rail they could manage, and then turned around and sold the land for enormous profits. They got subsidized by the government to build infrastructure they then owned privately. And once they owned it, they could charge whatever they wanted.

1869: The Transcontinental Railroad and Economic Geography

When the First Transcontinental Railroad was completed in 1869, it wasn't just an innovation of transportation. It was a complete restructuring of economic power and economic participation. Before railroads, economic activity was local or regional. After railroads, whoever controlled the rails controlled market access for farmers, manufacturers, and basically everyone across the nation.

Think about it. You're a farmer in Kansas. You grew wheat. The only way to get your wheat to market is the railroad. And there's one railroad. Maybe two if you're lucky. They can charge whatever they want, and you either pay it or watch your wheat rot. You have no bargaining power. None.

The railroad companies knew this. They set up rate structures that charged more for short hauls than long hauls, because short-haul farmers had no alternatives. They gave preferential rates to big shippers over small ones. They even owned grain elevators and warehouses, so they controlled storage too.

By the 1870s, railroads had become the first truly national corporations, and they'd figured out the playbook: use government subsidies to build monopoly infrastructure, then extract wealth from everyone who depends on it.

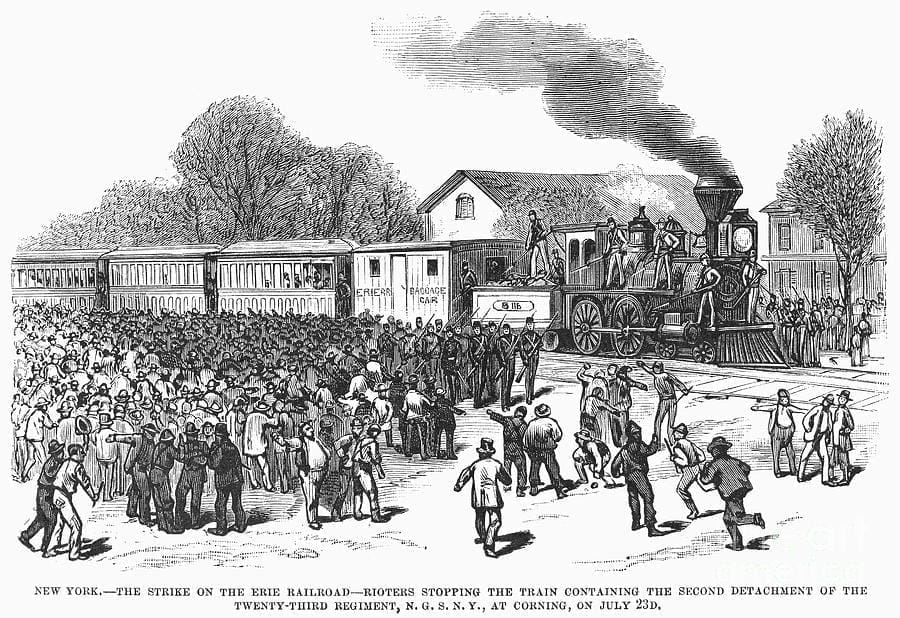

The Great Railroad Strike of 1877: When Government Picked Sides

Here's where things get really interesting. In 1877, railroad companies cut wages by 10% (they'd already cut them the year before). Workers in Maryland went on strike. Then West Virginia. Then it spread to Pittsburgh, Chicago, St. Louis, San Francisco. Within two weeks, you had the first nationwide strike in American history.

The railroad companies didn't negotiate. They didn't try to compromise. They called in the state militias. When that wasn't enough, President Hayes sent in federal troops. Not to mediate. To break the strike.

Over 100 workers were killed. Thousands arrested. The strikes collapsed. Wages stayed cut.

But here's what matters: this set a precedent that would echo for the next 150 years. When capital and labor conflict, the federal government uses force to protect corporate property. The railroads had proven they could get the government to deploy violence on their behalf.

Josh Hawley talks about this in "The Tyranny of Big Tech," and he's right to focus on it. The 1877 strike was the moment corporations learned they didn't just have economic power. They had the government's monopoly on violence backing them up.

The Gilded Age: How to Build a Monopoly (And Keep It)

The Trust Era: Standard Oil's Blueprint

By the 1880s, John D. Rockefeller had figured out something brilliant (if you're a monopolist). Instead of competing with other oil refiners, he'd just buy them. Or bankrupt them. Or both.

The Standard Oil Trust, formed in 1882, was the template. Here's how it worked: Rockefeller controlled about 90% of oil refining in the U.S. He negotiated special rates with railroads (because he shipped so much volume). These rates were so low that competitors couldn't match them. When competitors tried to undercut his prices, he'd sell at a loss in their region until they went bankrupt, then buy their assets for pennies on the dollar.

Oh, and he'd charge whatever he wanted once competition was eliminated.

Other industries watched and copied. Sugar, whiskey, lead, cotton oil. Trusts everywhere. By the 1890s, you had maybe a dozen men controlling the majority of American industrial output.

The Sherman Antitrust Act of 1890: A Law With No Teeth

Congress saw this happening and passed the Sherman Antitrust Act in 1890. It said you couldn't monopolize trade or commerce. Sounds great, right?

Except the law was vague as hell. It didn't define "monopoly" or "restraint of trade." It left everything up to interpretation. And guess who got to interpret it? Courts that were very friendly to business interests.

For the first decade, the Sherman Act was used more often against labor unions than against actual monopolies. I'm not making this up. Courts ruled that strikes and boycotts were "restraints on trade." But trusts? Those were just fine, apparently.

The law was symbolic. A way for politicians to say they'd done something without actually threatening corporate power.

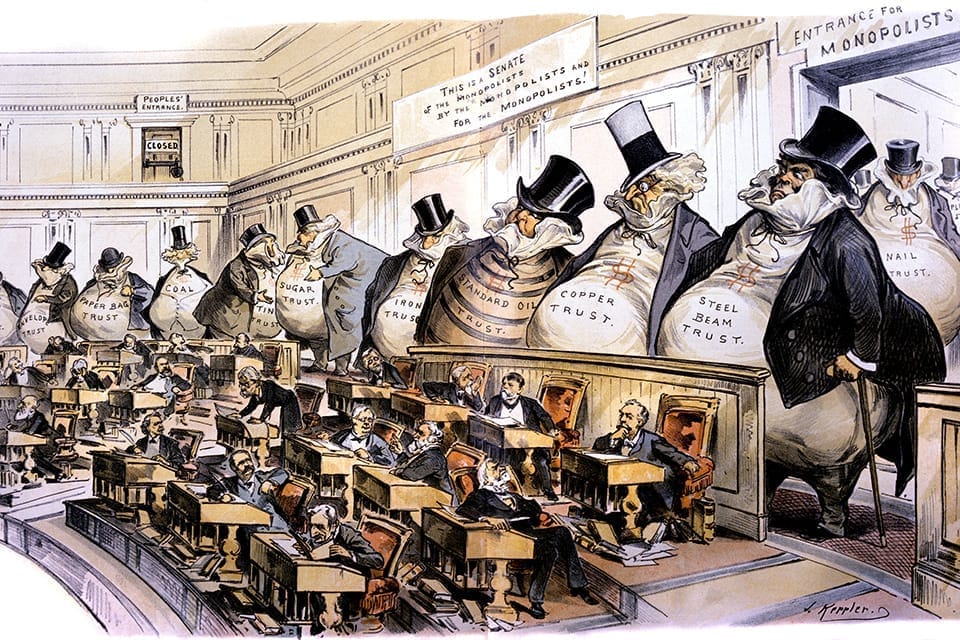

J.P. Morgan and the Consolidation Machine

If Rockefeller showed how to monopolize an industry, J.P. Morgan showed how to monopolize the entire economy.

Morgan's specialty was taking fragmented industries and merging them into giant corporations. He did this with steel (creating U.S. Steel in 1901, the first billion-dollar corporation). He did it with railroads (by 1900, he controlled about 60% of railroad mileage in America). He did it with electricity, telephones, shipping.

But here's the really important part: Morgan didn't just create these corporations. He sat on their boards. His partners sat on their boards. His banking competitors sat on their boards. The same small group of men controlled competing companies through interlocking directorates.

Why compete when you can collude? We see this today almost every company across every industry. We have the illusion of competition, yet all of these companies are owned and directed by the same financiers and board members. It's all a giant "Mega-Corp".

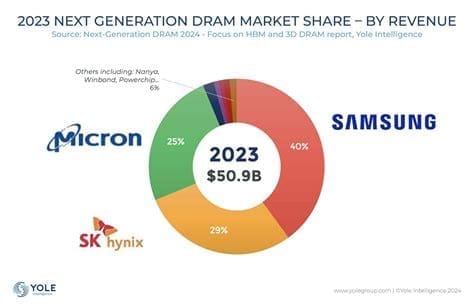

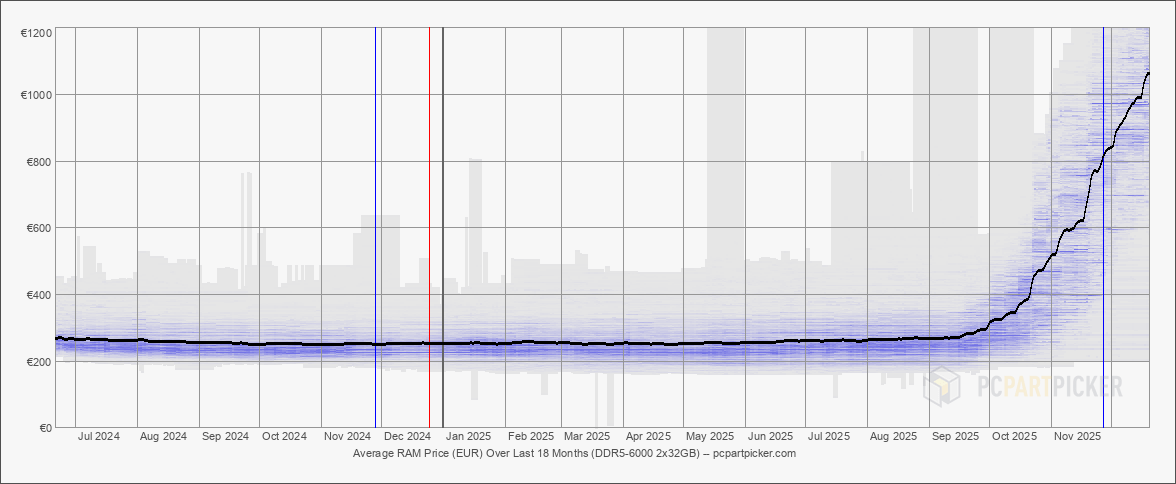

Three companies can dominate an industry. Take the RAM (Random Access Memory) industry for example. Micron, Samsung, and SK Hynix are the dominant producers of memory for nearly all computers and tech in the world. With a simple agreement (trust), they can artificially restrict supply and increase prices. They can even decide to drop consumer product lines like Micron's Crucial line. They can make it so that ordinary people simply cannot afford to build their own personal computers. They'll just have to rent a virtual computer in the cloud for $30/month!

Good thing that will never happen...

The Northern Securities Case: Trust-Busting Theater

In 1902, Morgan pushed things too far. He created Northern Securities Company, which merged competing railroad lines to create a total monopoly over transportation in the Northwest. Teddy Roosevelt, who actually believed in antitrust enforcement, sued.

In 1904, the Supreme Court broke up Northern Securities. Trust-busting! The little guy wins! Except... all the same people still controlled all the same railroads. They just did it through slightly different corporate structures.

The companies paid a small fine. Nobody went to jail. Business continued as usual.

This is a pattern you'll see again and again: when corporations get too blatant, there's a lawsuit or a new regulation, some executives testify before Congress, maybe a small fine gets paid, and then... nothing really changes. The same people control the same assets through slightly different mechanisms.

Keep in mind: fines for ordinary crimes are loopholes for the well-off and allow for additional government revenue (parking fines). Fines for corporations are loopholes for the elite to do what they want while contracting with the government for mutual benefit. The cost for the corporations to price fix or exploit is a fine to the government (cost of doing business), while the money they extract from the people exceeds the costs. It's a win-win for the government and the corporations.

The Money Trust: How Bankers Captured the Economy

The Pujo Committee Investigation (1912-1913)

By 1912, even Congress had to admit something was wrong. Representative Arsene Pujo chaired a committee to investigate the "Money Trust." What they found was stunning.

A small group of men (mostly Morgan and his associates, plus the Rockefellers and a few others) held 341 directorships in 112 corporations. These corporations controlled $22 billion in assets. That's the equivalent of about $600 billion in today's money, but more importantly, it was roughly one-third of all industrial capital in the United States.

The committee documented how this group controlled:

- Most major railroads

- Most major industrial corporations

- Most major banks and trust companies

- The New York Stock Exchange

- Access to credit for the entire economy

If you wanted to start a business, expand a factory, or build infrastructure, you needed capital. And to get capital, you needed these men's approval. They controlled who got loans, at what rates, and on what terms.

The Pujo Committee's report detailed exactly how this worked. These men didn't need to meet in smoke-filled rooms to coordinate. They sat on each other's boards. They socialized together. They married into each other's families. They had perfectly aligned interests.

One important detail: when these men controlled credit, they controlled which technologies succeeded and which failed. They funded railroads, steel, and banking. They didn't fund competitors to their existing businesses. Innovation that threatened their position got starved of capital.

This also applies today: The only technologies really funded and pushed is particle physics (CERN), AI technology, quantum computing, biology and longevity, genetics, nano-technology, nuclear fusion. What technologies do we not fund? Consciousness, imagination and intuition, the spiritual or immaterial, religious truth, kindness, love, plant intelligence/fungi, connection and community, ancient architecture or culture. It's clear that the Elite's are trying to become God. Certainly, they are not trying to improve communities and the lives of the entire civilization.

Pujo's committee recommended breaking up the money trust and regulating banking. Instead, Congress created the Federal Reserve. Well, technically Congress just passed the legislation. This critical failure will set the world on fire.

Jekyll Island, 1910: The Secret Design Meeting

Let me tell you about one of the weirdest moments in American financial history. In November 1910, a group of six men took a private train car from New York to Jekyll Island, Georgia. They traveled in secret, using only first names so nobody would know who they were. They spent ten days at a private club, and when they left, they'd drafted the blueprint for the Federal Reserve System.

Who were these men?

- Senator Nelson Aldrich (his daughter married John D. Rockefeller Jr.)

- Henry Davison (senior partner at J.P. Morgan)

- Frank Vanderlip (president of National City Bank, the largest bank in America)

- Paul Warburg (Kuhn, Loeb & Co., representative of Rothschild banking interests)

- Charles Norton (First National Bank)

- Benjamin Strong (Bankers Trust, later became first head of the New York Fed)

Notice anything? They're all bankers. Or politicians funded by bankers.

The meeting was kept secret for decades. Vanderlip wrote about it in his memoir in 1935: "There was an occasion, near the close of 1910, when I was as secretive—indeed, as furtive—as any conspirator... I do not feel it is any exaggeration to speak of our secret expedition to Jekyll Island as the occasion of the actual conception of what eventually became the Federal Reserve System."

Why the secrecy? Because if the public knew that the nation's central bank was being designed by the very bankers it was supposed to regulate, there would've been riots.

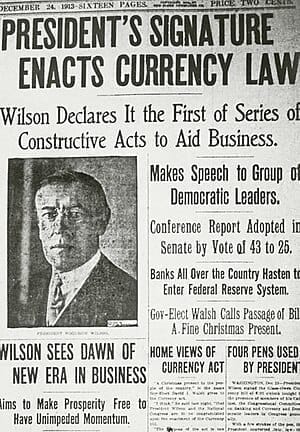

The Federal Reserve Act of 1913: Private Banking, Public Facade

On December 23, 1913 (the day before Christmas Eve, when most of Congress had already left Washington), the Federal Reserve Act passed. Woodrow Wilson signed it into law.

Here's what the Federal Reserve actually is: a network of private banks with government oversight. There are 12 regional Federal Reserve Banks, and they're owned by the member banks in their districts. Not by the government. By banks.

The Federal Reserve has the power to:

- Create money out of nothing

- Set interest rates

- Control the money supply

- Act as lender of last resort to banks

Now, the complicated part is that it's also accountable to Congress and the president appoints the Board of Governors. So it's this weird hybrid, technically private but functionally governmental. The genius of the design is that it can claim to be whatever is most convenient at any moment. Public accountability? It's a government institution. Profit and private control? It's owned by banks.

G. Edward Griffin lays this out in "The Creature from Jekyll Island," and while he gets conspiratorial about some things, the basic structure he describes is accurate. The Fed is a cartel of banks that was given government power to create money and set monetary policy.

Why does this matter? Because when you control the money supply, you control everything else. You control which sectors get credit and grow, which get starved and shrink. You control asset prices. You control inflation. You control who wins and who loses in the economy.

And here's the key insight: when new money enters the economy, it doesn't affect everyone equally. The people closest to the money printer benefit first. They can borrow at low rates before inflation kicks in, buy assets before prices rise, invest before others even know the money exists. By the time that money reaches regular workers through wages, prices have already increased.

This is called the Cantillon Effect (after Richard Cantillon, who wrote about it in the 1730s). The Fed's creation institutionalized this effect at the heart of the American financial system.

The 16th Amendment: Funding the New System

The Federal Reserve Act passed in December 1913. But something else happened earlier that year: the 16th Amendment was ratified in February, creating the federal income tax.

Why does this matter? Because the Federal Reserve system required a permanent revenue source for the government. Here's how it works:

The government spends money (on wars, programs, whatever). It borrows money by issuing Treasury bonds. The Federal Reserve buys those bonds (with money it creates). The government now owes interest on those bonds. Where does it get money to pay the interest? Taxes.

Before the income tax, the federal government ran on tariffs and excise taxes. These hit imported goods and luxury items, which meant the wealthy paid most of the taxes. The income tax shifted the burden to wages. Now everyone with a job pays a portion directly to the federal government.

Think about the timing. Federal Reserve created in December 1913. Income tax created in February 1913. Both in the same year. That's not a coincidence.

The system needed both pieces. The Fed to create money and buy government debt. The income tax to ensure the government could service that debt.

World War I: The First Modern Money Printing

Financing the War (1914-1918)

When World War I started in Europe in 1914, the U.S. stayed neutral for three years. But in April 1917, America entered the war. And wars are expensive. Really expensive.

The total cost of U.S. involvement was about $27 billion (around $600 billion in today's money). About half of that was financed through Liberty Bonds, which the Federal Reserve promoted and banks bought. The other half? The Fed just created the money.

From 1914 to 1918, the money supply in the United States tripled. It went from $5.4 billion to $17.7 billion. That's not a gradual increase from economic growth. That's straight up money printing.

What happened next is what always happens when you print money: inflation. Consumer prices increased about 70% during the war years. If you were a saver, your money lost most of its value. If you were a worker on fixed wages, your real income collapsed. If you were a bank that had just lent out all that new money? You made a fortune.

This was the first real-world demonstration of what the Federal Reserve could do. It could finance a war without raising taxes proportionally. It could create money to buy government debt. It could inflate away the real burden of that debt. And the costs would be distributed across everyone who held dollars, while the benefits went to banks and government.

After WWI ended, there were calls to abolish the Fed. People had seen what it could do, and they didn't like it. But by then, the system was entrenched. The banks that owned the Fed made sure it wasn't going anywhere.

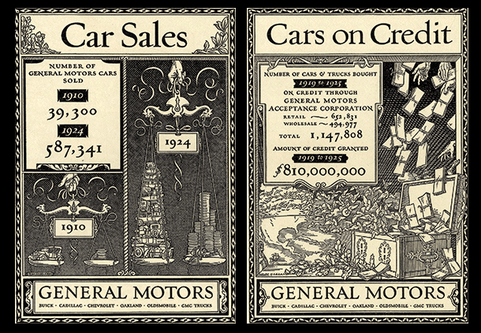

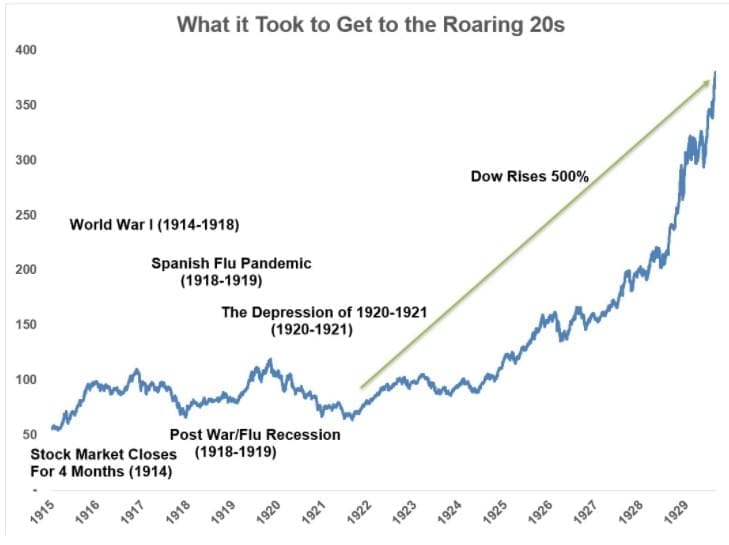

The 1920s: Speculation and the Coming Crash

The Roaring Twenties and Easy Credit

After a sharp recession in 1920-21 (as the war economy contracted), the Fed flooded the system with cheap credit. By the mid-1920s, you could borrow money at incredibly low rates. And people did.

The stock market became a casino. Margin buying became normal. You could buy $100 of stock with $10 down and borrow the other $90. When stocks went up, you made ten times your money. When they went down... well, that was a problem for later.

Banks were making speculative loans like crazy. Why? Because the Fed would bail them out if anything went wrong. The lender of last resort feature wasn't just a safety net. It was moral hazard. Banks could take huge risks because they knew the Fed had their backs.

Meanwhile, the real economy was struggling. Agricultural prices had collapsed after the war. Farmers were going bankrupt throughout the 1920s. But that didn't matter to Wall Street. The stock market kept going up.

From 1924 to 1929, bank credit expanded from about $17.7 billion to $26.4 billion. Stock prices tripled. Everyone was getting rich. On paper.

Corporate Profits and Wealth Concentration

Here's something that gets forgotten about the 1920s: corporate profits soared, but wages didn't. The gains from economic growth went almost entirely to investors and executives.

The top 0.1% of earners saw their share of national income reach 10% by 1929. That's a level of inequality that wouldn't be seen again until... well, until now, actually. We're back at 1920s levels of wealth concentration.

Companies were doing stock buybacks (legal at the time), paying huge dividends, and enriching shareholders while keeping worker pay flat. The productive capacity of the economy was growing, but purchasing power wasn't keeping up.

This is important because it set up the crash. When the bottom 90% of people don't have money to buy goods, eventually demand collapses. But nobody saw it coming because stock prices kept rising.

The Great Depression: When the System Broke (Temporarily)

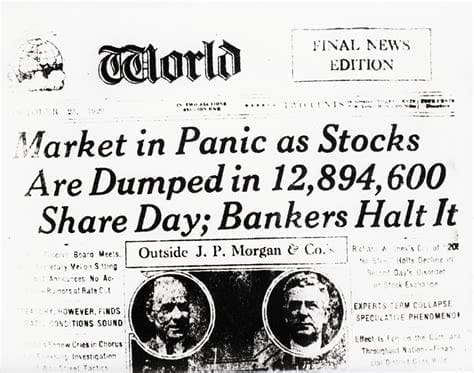

October 1929: The Crash

On October 24, 1929 (Black Thursday), the stock market collapsed. Investors who'd bought on margin got wiped out. Banks that had lent money for stock speculation couldn't get repaid. The whole pyramid scheme came down.

Over the next three years, about 9,000 banks failed. A third of all banks in the country. When a bank failed, depositors lost everything. There was no FDIC insurance yet.

GDP fell 30% from 1929 to 1933. Unemployment hit 25%. Industrial production fell by half. Millions of people lost their homes, their savings, their jobs.

And here's the thing: the Federal Reserve made it worse. Instead of creating money to prevent deflation, they contracted the money supply. Banks needed liquidity, and the Fed let them fail. The very institution created to prevent financial panics stood by and watched the worst financial panic in American history.

Why? There are debates about this, but the simplest explanation is that the New York Fed (controlled by big banks) wanted to let smaller banks fail so they could buy up the assets. Consolidation through crisis.

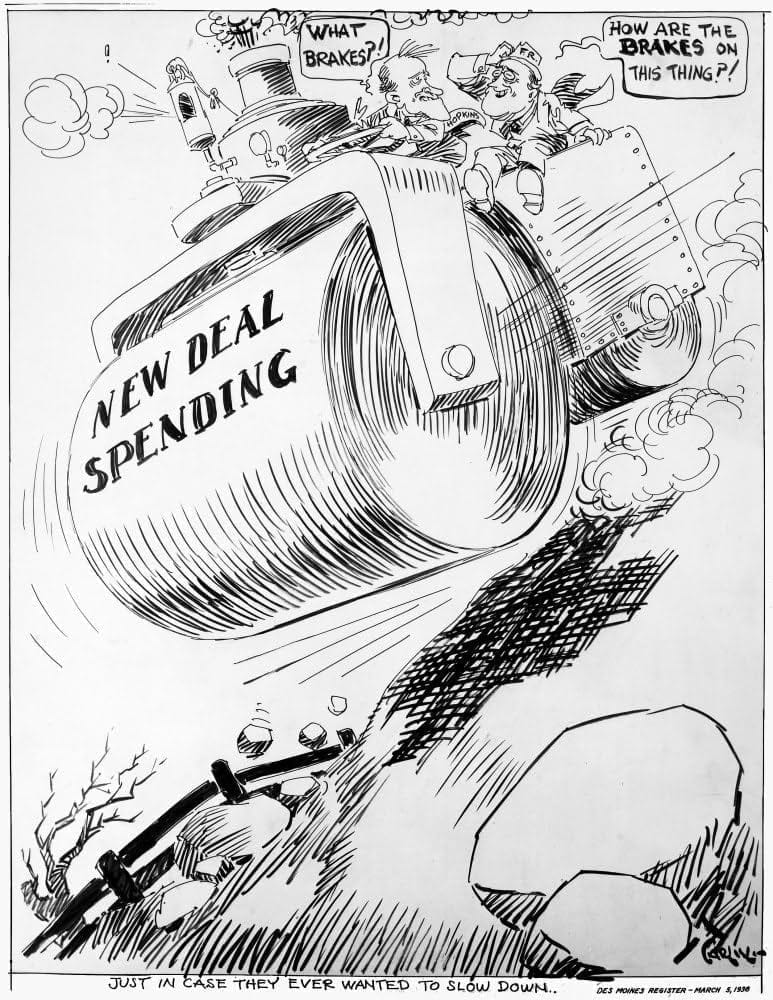

Roosevelt's Response: The New Deal (1933-1938)

When Franklin Roosevelt took office in March 1933, he had to do something. Fast. The entire financial system was collapsing.

His first act was to declare a bank holiday. He closed every bank in the country. Then he passed the Emergency Banking Act, which gave the government power to inspect banks and only reopen the solvent ones. This restored some confidence.

Then came the real changes:

Glass-Steagall Act (1933): This separated commercial banking from investment banking. The idea was simple: banks that take deposits from regular people shouldn't be allowed to gamble with that money on Wall Street. You want to speculate? Fine, but not with insured deposits.

This worked, by the way. From 1933 to 1999 (when it was repealed), there were no major banking crises. But I'm getting ahead of myself.

Banking Act of 1935: This gave the Federal Reserve more centralized control. Before this, the 12 regional Fed banks operated semi-independently. After 1935, the Board of Governors in Washington had more authority. This made the Fed more powerful and more political.

Social Security Act (1935): So in 1935 they created Social Security, but here's what nobody wants to say out loud: it wasn't really about protecting retirees. Think about what actually happened. The government required every worker to get a number and start paying FICA taxes. Every single person became a line item on a spreadsheet, a predictable revenue stream they could calculate and borrow against.

Your FICA taxes? They don't go into some account with your name on it. That money goes straight out the door to pay current retirees. Your future benefits become someone else's problem, another generation's debt to service. It's just aggregate cash flows that let the government issue bonds backed by, get this, your productive capacity. The "full faith and credit" clause suddenly meant something very specific: your labor.

And that Social Security number changed everything. You weren't a citizen anymore in the old sense, autonomous and anonymous. You became asset #123-45-6789 on the federal balance sheet. Trackable. Taxable. Quantifiable. The government could now project your lifetime earnings, estimate your tax contributions, and structure their borrowing around those numbers.

It's an inter-generational debt scheme dressed up as insurance. Your labor subsidizes today's spending while creating claims against workers who aren't even born yet. Pretty elegant financial engineering, if you think about it. Also pretty dystopian.

This created a new form of government dependency. Once people expected Social Security, they'd vote for politicians who protected it. The system locked in its own political constituency.

Gold Confiscation and Dollar Devaluation

In 1933, Roosevelt issued Executive Order 6102, which required Americans to turn in their gold to the government. Holding gold became illegal (with small exceptions for jewelry and collectibles). The government paid $20.67 per ounce.

Then, in 1934, the Gold Reserve Act revalued gold to $35 per ounce. So the government forced people to sell at $20.67, then immediately revalued it to $35. That's about a 70% confiscation of wealth from anyone who'd saved in gold.

Why did they do this? Because gold limits money printing. If people can redeem dollars for gold, you can't create unlimited dollars. But if the government owns all the gold and can change its dollar price whenever it wants, there's no limit.

This set up the post-WWII system where only foreign central banks could redeem dollars for gold. Regular citizens? You got paper dollars, and you'd better like it.

The Fair Labor Standards Act (1938)

In 1938, Congress passed the Fair Labor Standards Act, which created the federal minimum wage, the 40-hour work week, and overtime pay requirements. It also banned child labor.

The minimum wage and child labor provisions are fine. But here's what else the law did: it federalized employment regulations. Before 1938, states set their own labor laws. After 1938, the federal government controlled wages and hours nationwide.

This shifted power from local jurisdictions (where workers and employers lived) to Washington D.C. (where lobbyists operated). It made employment rules more uniform but also more subject to regulatory capture by large corporations that could afford compliance costs.

Small businesses and local economies lost flexibility. Big corporations gained the ability to influence rules that applied to their competitors nationwide.

World War II: Permanent Debt State

Financing the War (1941-1945)

If WWI showed what the Fed could do, WWII proved it would never go away. The war cost about $300 billion in 1940s dollars (roughly $4 trillion today). The national debt went from $43 billion in 1940 to $260 billion in 1945. A six-fold increase in five years.

The Fed bought huge quantities of Treasury bonds. They kept interest rates artificially low so the government could borrow cheaply. They created money on a scale that made WWI look tiny.

And something interesting happened: massive inflation didn't occur immediately. Why? Because the government also imposed price controls, rationing, and wage controls. They literally made it illegal to raise prices. So the inflation was suppressed during the war, but all that money was still sloshing around in the system.

After the war ended and controls were lifted, prices jumped. But by then, the debt had been inflated away. The government borrowed in 1942 dollars and paid back in 1946 dollars that were worth less. Savers and bondholders got screwed. The government got a free war.

The Military-Industrial Complex

During WWII, the federal government became the largest customer for American industry. Aircraft manufacturers, steel companies, chemical companies, electronics firms... they all depended on military contracts.

After the war, they didn't want that gravy train to end. Neither did the military brass, who liked having cutting-edge equipment. Neither did the politicians, who liked having jobs in their districts.

Eisenhower warned about this in his farewell address in 1961 (I know, that's outside our timeframe, but the groundwork was laid in WWII). He called it the military-industrial complex. A permanent fusion of military, corporate, and government interests that would push for endless military spending regardless of actual threats.

This matters because it created a constituency for government debt. Defense contractors wanted spending. Banks wanted to lend. The Fed could print money to buy the bonds. Everyone in the system benefited except taxpayers and savers.

Post-War: America's New Position

When WWII ended, America held about two-thirds of the world's gold reserves. Every other major economy was destroyed. European factories were rubble. Japan was occupied. The Soviet Union had lost 27 million people.

America was the only major industrial economy left standing. And it had a central bank that could create dollars at will, backed by the world's largest gold reserves and the world's most powerful military.

This set up the Bretton Woods system, which we'll get to in Part 2. But the key point is that WWII cemented America's position as the center of the global financial system, with the Federal Reserve at the heart of it.

What Was Built: A System of Concentrated Control

So let's pause and look at what got created between 1830 and 1945:

Corporate Power: Corporations went from state-chartered entities with public purposes to private organizations with government-protected monopolies. They learned to use government force against workers and competitors. They consolidated industries through trusts, mergers, and interlocking directorates.

Financial Control: A small group of bankers gained control over credit allocation for the entire economy. They designed the Federal Reserve to legalize and perpetuate this control. They could create money, set rates, and decide which sectors got funded.

Government Expansion: The federal government went from minimal peacetime functions to massive economic intervention. It gained the power to tax income, create money through the Fed, regulate employment, control prices, and finance unlimited spending through debt.

Debt Dependence: The economy became based on debt instead of savings. The government ran permanent deficits financed by Fed money creation. Corporations borrowed to expand. The average person's purchasing power got inflated away.

Interlocking Interests: Banks, corporations, and government became mutually dependent. Banks needed government protection and Fed bailouts. Corporations needed government contracts and favorable regulations. Government needed banks to buy its debt and corporations to fund political campaigns.

By 1945, you had a structure where:

- A few dozen men controlled most major corporations

- Those same men controlled the banking system

- The banking system controlled the money supply through the Fed

- The government depended on the Fed to finance its spending

- Regular people's savings got inflated away to pay for all of it

This wasn't capitalism in any meaningful sense. It was a managed economy run by and for financial elites, with government providing the legal and military backing. (I am in the process of researching alternative applicable definitions of our economy, and it's not quite "capitalism" — at least not "free market capitalism.")

And this was just the foundation. In Part 2, we'll see how this system expanded globally after WWII, how the wage-productivity relationship broke down after 1971, and how deregulation in the 1980s-90s concentrated power even further.

But you can already see the pattern, right? Each crisis led to more centralization. Each reform made the system more complex and less accountable. Each generation inherited a more captured economy than the last.

The railroad monopolies of the 1870s were regional. The trusts of the 1890s were national. The banking cartel of the 1910s was centralized. By 1945, you had a globally dominant financial system with the Fed at the center.

And Gen Z wonders why they can't afford a house.

The foundation was laid more than a century ago. What happened next just built on it.

Next: Part 2 will cover 1945-2000, where we'll see the Bretton Woods system, the crucial 1971 Nixon Shock that changed everything, the wage-productivity divorce, Reagan-era deregulation, the legalization of stock buybacks, and how the internet created a new form of corporate control. That's where things really accelerate.

Helping you achieve digital sovereignty through open-source solutions and human-centered AI automation.

Self-Hosting + Privacy + Automation

nick@apalto.ai